How to Make the Most of the Annual Gift Tax Exclusion

The holidays often inspire a spirit of generosity. So, at year end, many people decide to give money or assets to their loved ones. Over time, lifetime gifts can also be an effective way for wealthy people to minimize their taxable estates. Here are the basic federal tax rules for these transactions.

Beware: Quite a few states impose estate or inheritance tax at a lower threshold than the federal government does. So it’s also important to understand the rules in your state to avoid an unexpected tax liability or other unintended consequences of an asset transfer.

Estate and Gift Tax Basics

Currently, the unified federal estate and gift tax exemption shelters from tax up to $10 million of transfers at death or during your lifetime, indexed for inflation. For 2021, this figure is $11.7 million, or effectively $23.4 million for married couples. For 2022, it will increase to $12.06 million ($24.12 million for married couples). Those amounts are generous by historical standards.

Estates worth more than the current unified federal estate and gift tax exemption are exposed to the federal estate tax at rates as high as 40%. So, wealthy individuals may need to take steps to reduce their exposure.

Unfortunately, in 2026, the unified exemption is set to fall to about $6 million, or $12 million for married couples, after inflation adjustments — unless Congress changes the law sooner. However, changes to the estate and gift tax rules are not part of the most recent edition of the Build Back Better bill that’s currently being debated by Congress.

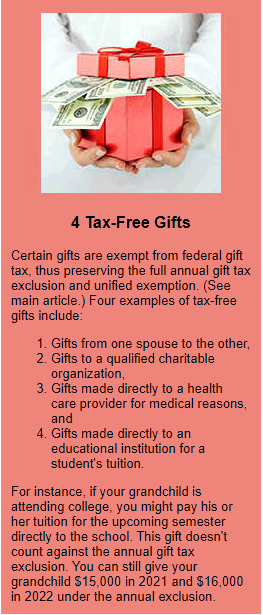

The annual gift tax exclusion provides tax shelter without eroding any part of the unified exemption. Under the annual exclusion, you can give each recipient up to a limit each year with zero gift tax liability. For 2021, the annual exclusion is $15,000 per recipient. For 2022, it will increase to $16,000 per recipient.

For example, say that you have three adult children and seven grandchildren. Thanks to the annual gift tax exclusion, in 2021 you can give each of these family members $15,000 — a total of $150,000 — without owing any gift tax. The gifts also reduce your taxable estate by $150,000.

To maximize these tax benefits, give $15,000 to each recipient in December 2021, then give $16,000 to each recipient in January 2022. In the preceding example, you could gift a total of $310,000 ($150,000 in December plus $160,000 in January) without owing any federal gift tax. Repeating this strategy over many years can be an effective way to minimize your taxable estate.

Gifts above the annual exclusion may count toward your unified federal estate and gift tax exemption without triggering federal gift tax. But this will reduce the available estate tax shelter.

The Art of Gift Splitting

It’s also important to point out that the annual exclusion is available to each taxpayer. That means if you’re married, your spouse can join in the gift — often called “gift splitting” — or you can give separate gifts. With gift splitting, the annual exclusion is effectively doubled. In the preceding example, gift splitting would enable a married couple to give away $620,000 to ten family members ($310,000 times 2) in a short time span.

But there’s a catch: When you give gifts under the annual exclusion on your own, you don’t have to file a federal gift tax return. Generally, a return is only required if you exceed the maximum exclusion amount, whether or not you dip into the unified exemption. However, if you’re gift splitting, you must file a gift tax return for that year, even if you don’t exceed the maximum annual gift tax exclusion amount.

Also, there’s no “joint gift tax return.” So each spouse must file an individual federal gift tax return for the year in which they both make gifts.

The deadline for the gift tax return is April 15 of the year following the year of the gift, the same as the due date for income tax returns. (The deadline is moved to the next business day if it falls on a weekend or holiday.)

So, for gifts made in 2021, you must file your gift tax return by April 15, 2022. However, if you extend your income tax filing to October 17, 2022, this extension also applies to your gift tax return.

Important: Even if you’re not required to file a gift tax return, you may choose to do so anyway. This establishes the value of assets with the IRS. A safe-harbor rule says that if you disclose a legitimate value for the gifts on Form 709, “United States Gift (and Generation-Skipping Transfer) Tax Return,” your return can’t be audited after three years — and the IRS is prohibited from revisiting the issue in any subsequent audit of your estate.

What’s Your Plan?

There’s more to gift-giving than meets the eye. Remember that you’re relinquishing control over the assets you’re gifting, so you may not always want to take this approach. Consider other alternatives, such as trusts or intrafamily loans, that may better meet your objectives.

However, if you’re willing to lose control of the assets, a multi-year gifting strategy is probably the simplest and most convenient method for passing assets to loved ones without any federal tax consequences. Future earnings from the assets are then taxed to the recipients who are presumably in lower income tax brackets than yours. Contact your tax advisor to develop a systematic plan for giving lifetime gifts that maximizes the benefits of the annual gift tax exclusion.

*This article comes from Walz Group’s December 1st, 2021 issue of The Bottom Line.